NZSA Disclaimer

It’s hard to believe KiwiSaver is now old enough to vote. Having just turned 18, it’s moving beyond its “teenage” years into something resembling financial adulthood.

July 2007 seems like such a long time ago.

And like any young adult, it’s showing signs of independence and maturity.

From $28.5 billion spread across 2.5m members in March 2015, KiwiSaver now has close to $130 billion under management for 3.3m members as at June 2025 (Morningstar). That’s underpinned a massive increase in New Zealand’s household savings rates. By 2030, according to at least one provider, KiwiSaver funds are likely to reach $200 billion.

The growth is not just down to increasing member contributions. The power of compounding returns is oft said to be the eighth wonder of the world, a fact not lost on savvy investors. While it’s difficult to source overall figures, the estimated return for a typical ‘aggressive’ KiwiSaver fund is likely to range between 8.0% – 9.5% per annum over the last 10 years, with a ‘conservative’ fund returning 3.5% – 4.5%.

KiwiSaver’s influence has gone beyond account balances. It’s shifted our investing culture; a BBQ conversation about investment has become much less of a taboo subject as the growth in KiwiSaver assets has impacted nearly all New Zealand households, supported by the regular contributions featured on every payslip. While financial literacy challenges remain, KiwiSaver has created a national baseline for engagement with money and investment.

KiwiSaver is a key element of the pathway for retirement funding. Alongside the NZ Superannuation Fund (NZSF), KiwiSaver provides support to government in extending the life of New Zealand’s universal pension for those over 65. Right now, over 65’s comprise nearly 15% of our population, a figure projected to increase to over 20% over the next two decades. At one point, unpopular as it may be, future governments will have no choice but to address this issue as both inflation and an aging population place ever more pressure on the tax base. Gradual, transparent change will be essential to protect those close to retirement.

The global view

The universal approach in New Zealand is similar to countries like Norway and Sweden – but we remain a global outlier. Our favourite neighbour, Australia, also offers a pension to its residents, although this is subject to means testing.

The Australian equivalent to KiwiSaver began in 1992, giving it a 15 year head start. It also offers significantly higher employer contribution rates (12% compared to 3% for KiwiSaver). This has created a $4.2 trillion behemoth representing average savings of nearly AU$150,000 for every Australian (New Zealand: a mere NZ$22,500).

Crikey.

A changing investment culture

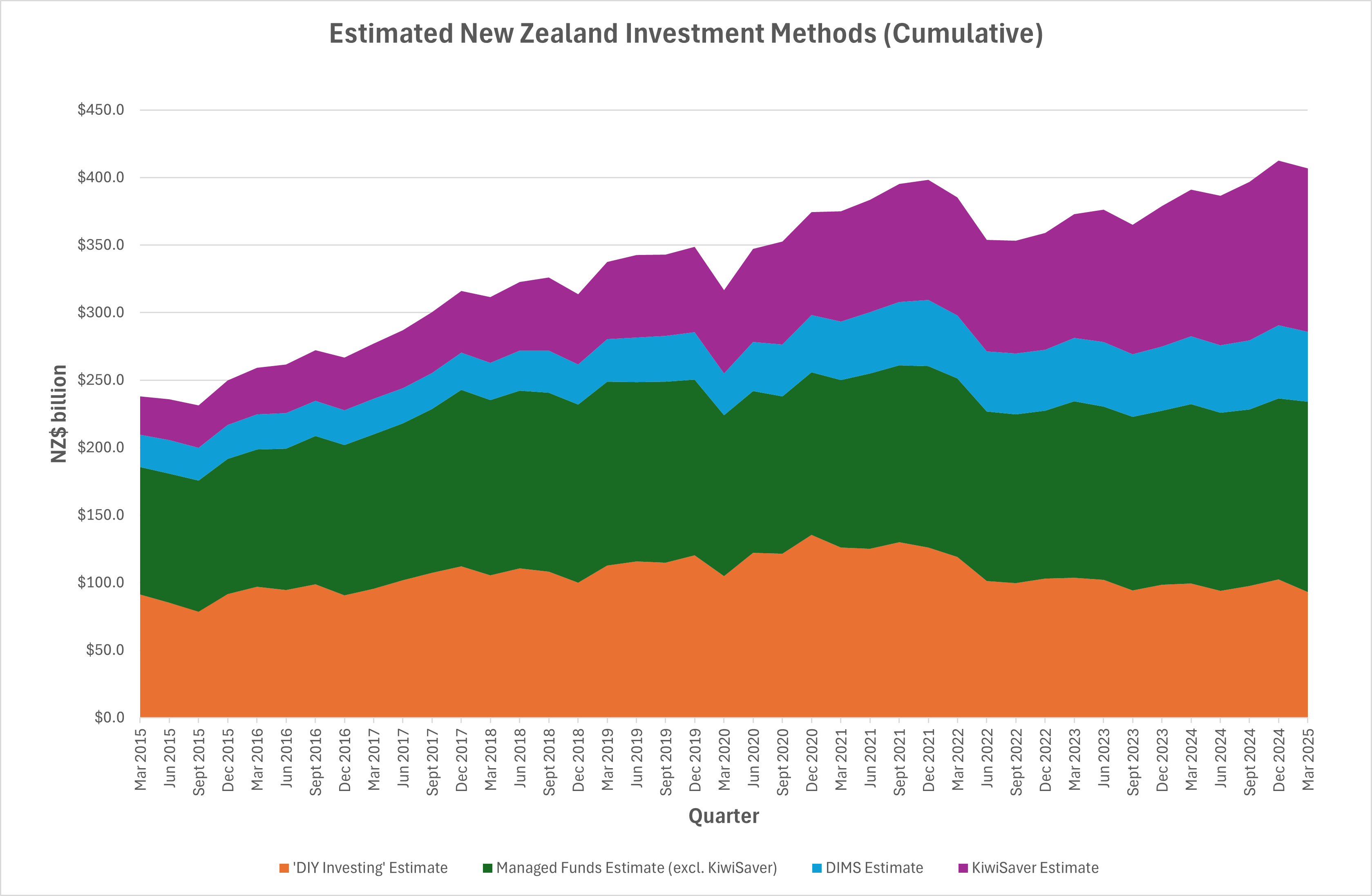

Over the last decade, it isn’t just KiwiSaver that has grown massively. The rise of funds, whether exchange-traded or offered by a growing cohort of fund managers, and the “discretionary investment management service” (DIMS) provided by wealth managers have changed the game for Kiwi investors.

This offers options for all. A ‘DIY’ investor making their own investment decisions requires both interest and capability, while a DIMS approach is a means of ‘outsourcing’ investment decisions to professionals (for a fee, of course). In between those extremes, a fund investment allows an investor to select an investment strategy and/or approach, without getting into the detail of stock-picking.

The data shows some clear shifts.

The first is the rise and rise of KiwiSaver. We may not quite be at the scale of Australian Superannuation, but the magic of compounding, increasing contribution rates and the inclusion of nearly all New Zealand employees has resulted in KiwiSaver becoming the ‘anchor’ for household investing.

Secondly, traditional ‘DIY’ investing has fallen from an estimated 38% of investment funds in March 2015 to around 23% today (and possibly lower, depending on how wealth manager services are provided).

On this basis, retail investment would appear to be a dying art.

But not all is lost – in terms of absolute numbers, if not value, the rise of Sharesies has encouraged a whole new generation of New Zealanders to be interested in investment, even if this is not yet reflected in overall ‘dollar value’. Other ‘execution-only’ platforms, such as Invest Direct and ASB Securities, also support the efforts of DIY investors.

Last , wealth managers have increasingly channelled investors towards more lucrative services – such as an in-house fund or a DIMS approach.

Ultimately, the development of investment options to suit all Kiwis will help our national investment profile for years to come.

KiwiSaver providers

There are now 38 licensed KiwiSaver providers in New Zealand, with 6 providers as “default” providers (Simplicity, BNZ, Booster, Fisher Funds, Westpac and Smart). Default providers allow Inland Revenue to assign employees who have not selected a provider to one of the default schemes.

The rising investment capability of New Zealanders shows up in two key trends when it comes to KiwiSaver.

The rise of specialist providers: Over the last decade, the collective market share of bank-aligned providers has declined in favour of specialist providers, like Generate and Milford Asset Management. In the June 2025 quarter, these two attracted the largest net inflow, while ASB Bank suffered the largest outflow. Despite this trend, ANZ Bank remains the largest provider, with an 18% market share.

Move towards higher growth funds: In early 2015, conservative funds represented around 43% of KiwiSaver assets. By 2024, that had dropped to 17%, with growth funds climbing from 26% to 46%. More Kiwi investors are taking on risk for higher potential returns over the long haul.

Making a choice

In selecting a KiwiSaver fund, more are making a conscious choice as to the fund they wish to invest in. The list below does not constitute investment advice, but may be helpful in thinking about your options when it comes to selecting both a provider and a fund.

- Make an active choice – even if it is to stay with the default provider, this is still a choice!

- Check out the net investment performance (ie, after fees) – but look at this over the long-term, not just the last year.

- Understand the fees charged by providers. Even small differences in fee structures compound over time.

- Understand your own objectives and time frames to retirement – and when you need to access your KiwiSaver funds after retirement.

- Look at how a provider aligns with your own values – and the disclosure that supports that.

- Understand how a provider interacts with the companies in which they invest. This may be as simple as voting in company meetings, but may also extend to other forms of “active stewardship”.

Oliver Mander