If you’re not yet a member, join now for access to a whole lot more!

7 April 2026

Accordant Group Ltd (AGL)

Meeting Date: Thursday 16 April 2026

Venue: It will be a virtual meeting. You can join the meeting online at this link.

Company Overview

The company operates under the following banners:

- AWF supplies skilled and semi-skilled workers to the infrastructure, transport and logistics, manufacturing, technical and construction sectors.

- Madison recruits for professional roles and managerial positions.

- AbsoluteIT provides workers to the technology and digital sectors.

- JacksonStone & Partners is an executive search and recruitment consultancy and a member of the CFR Global Executive Search alliance.

- The Work Collective an employment initiative connecting Employers, Employment Support organisations and the company. The purpose is to provide meaningful work opportunities for those who face barriers to employment.

- Hobson Leavy a long-established executive search firm, acquired by Accordant in January 2023.

Current Strategy

The strategy is to be New Zealand’s leading recruitment and resourcing company.

Purpose of meeting.

This is a Special Shareholders Meeting to approve resolutions to allow the company to raise new capital.

Disclaimer

To the maximum extent permitted by law, New Zealand Shareholders Association Inc. (NZSA) will not be liable, whether in tort (including negligence) or otherwise, to you or any other person in relation to this document, including any error in it.

Forward looking statements are inherently fallible.

Information on www.nzshareholders.co.nz and in this document may contain forward-looking statements and projections. For any number of reasons, the future could be different – potentially materially different. For example, assumptions may be wrong, risks may crystallise, unexpected things may happen. We give no warranty or representation as to any future financial performance or any other future matter. We may not update our website and related materials for changes.

There is no offer or financial advice in our documents/website.

Information included on www.nzshareholders.co.nz and in this document is for information purposes only. It is not an offer of financial products, or a proposal or invitation to make any such offer. It is not financial advice and does not take into account any person’s individual circumstances or objectives. Prior to making any investment decision, NZSA recommends that you seek professional advice from a licensed financial advice provider.

There are no representations as to accuracy or completeness.

The information, calculations, and any opinions on www.nzshareholders.co.nz and in this document are based upon sources believed reliable. The NZSA, its officers and directors make no representations as to their accuracy or completeness. All opinions reflect our judgement on the date of communication and are subject to change without notice.

Please observe any applicable legal restrictions on distribution

Distribution of our documents and materials on www.nzshareholders.co.nz (including electronically) may be restricted by law. You should observe all such restrictions which may apply in your jurisdiction.

Context

The company has experienced several difficult years with losses of $10 million in FY24 and $2.9 million in FY25. The proposed renounceable rights offer will seek to raise up to approximately $6.7 million of equity by granting a right to eligible shareholders to subscribe for 1.269 new shares for every 1 existing share held, at a price of $0.15 per new share.

The proceeds from the offer will be used to reduce AGL’s indebtedness. The company will continue to maintain a focus on cost control and profitability going forward as it looks to benefit from more favourable economic trading conditions which are expected in the mid-term.

Shareholders are being asked to vote on two resolutions.

- Only the first resolution (which relates to subscription for new shares by AGL’s founder and major shareholder, Simon Hull) is required to be passed for the rights offer to open.

- The second resolution, if passed, will assist the rights offer by allowing related parties to apply for new shares not taken up by other applicants in the shortfall facility if they would otherwise be prevented from doing so under the NZX listing rules.

The dilutionary impact of the Rights Offer on a Shareholder will depend on the extent of that Shareholder’s participation in the Rights Offer as well as that of other Shareholders and investors. If a Shareholder did not (or was ineligible to) exercise their Rights at all, or sold their Rights, their percentage shareholding in AGL would be significantly diluted as a result of the Rights Offer

The company has commissioned Simmons Corporate Finance to prepare an independent Report and a copy of this is included with the Notice of Meeting. The Report concludes “In our opinion, after having regard to all relevant factors, the terms and conditions of the Related Parties Allotments are fair to the Company’s shareholders not associated with the Related Parties (the Non-Related Parties-associated Shareholders).”

The full details of the capital raise are included in the Notice of Meeting and accompanying investor presentation.

NZSA Commentary

Offer Structure: NZSA notes the ‘AREO’ structure, with all shareholders being able to participate and oversubscribe for a shortfall allocation on the same terms. The rights will be tradeable on-market, allowing the potential for shareholders to realise some value if they are unable and/or unwilling to participate. There is no ‘bookbuild’ process, with any shortfall allocation being issued at the offer price.

The offer is not underwritten.

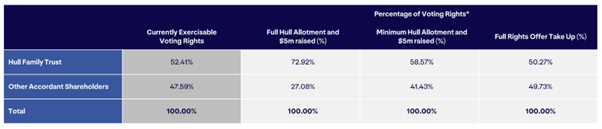

Majority owner: The Hull Family Trust owns approximately 52.4% of AGL. Simon Hull is also a Director of AGL. The Trust will take up rights slightly less than its entitlement, but reserves the right to participate in the shortfall allocation process. If all rights are taken up, the Hull shareholding will reduce slightly to 50.3% – still in excess of the 50% threshold required for Hull Family control.

Financial Outcomes: The share offer is being carried out at a significant discount to both the previous trading price (approximately 50%) and at the theoretical ex-rights prices (about 32% versus the $0.22 TERP). For non participating shareholders, this results in significant dilution.

However, NZSA notes the most recently disclosed financial position of the company, announced to market during November 2025. This showed a half-year loss of $1.1m, continuing a period of losses in recent years. Of more concern was an increase in the already-high debt/equity ratio to 2.85 (as at Sep 2025) from 2.67 in March 2025. For context, this same ratio was only 1.25 in March 2021, with the change in AGL’s fortunes closely tied to the overall New Zealand economy.

Contingent on a successful capital raise, the company has secured an extension to its banking facility to April 2028, with revised banking covenants based on cumulative EBITDA, leverage ratio and interest cover ratios. This re-financing is of significant value for Accordant.

Outlook: Shareholders will need to make an active assessment as to their investment decision. The company has provided information that shows significant improvement in future years. If this comes to pass, this will likely translate to future value for shareholders.

Resolutions

1. The Hull Family Trust’s participation. To consider and, if thought appropriate, pass the following ordinary resolution:

That, the issuance of up to 31,431,983 New Shares to Simon Alexander Hull and David John Graeme Cox as trustees for the S.A. Hull Family Trust No. 2 (Hull Family Trust) for $0.15 per New Share pursuant to the Rights Offer, where such issue will cause the Hull Family Trust, as holders and controllers of more than 20% of AGL’s voting rights, to increase such holding and control, as described in the Notice of Meeting dated 30 March 2026, be approved under Rule 7(d) of the Takeovers Code.

This resolution requires approval as an ordinary resolution under Rule 7(d) of the Takeovers Code. See Explanatory Note 1 in Section 6 “Explanatory Notes”.

We will vote undirected proxies IN FAVOUR of this resolution.

2. Related Parties’ participation. To consider and, if thought appropriate, pass the following ordinary resolution:

That, subject to Ordinary Resolution 1 being passed, the issuance of New Shares to one or more Related Parties for $0.15 per New Share pursuant to the Rights Offer, up to the number of Remaining Shortfall Shares required to reach the Minimum Amount and, if greater, an additional number of Remaining Shortfall Shares to satisfy the Committed Related Party Subscription, as described in the Notice of Meeting dated 30 March 2026, be approved for all purposes, including under NZX Listing Rule 5.2.1.

This resolution requires approval as an ordinary resolution under NZX Listing Rule 5.2.1. See Explanatory Note 2 in Section 6 “Explanatory Notes”.

We will vote undirected proxies IN FAVOUR of this resolution.

Proxies

You can vote online or appoint a proxy at https://nz.investorcentre.mpms.mufg.com/voting/AGL

Instructions are on the Proxy/voting paper sent to you.

Voting and proxy appointments close 3.30pm Tuesday 14 April 2026.

Please note you can appoint the Association as your proxy. We will have a representative attending the meeting.

The Team at NZSA